Why China’s stunning vaccine surge could be good news for the world

Not only is the rapid roll-out of Covid-19 vaccinations in China good news for the domestic economy, but it could also potentially see a sharp increase in exports of treatments to other emerging markets (EM).

That would help those EM that have so far lagged behind in the vaccination race. And the geopolitical dynamics could also see the G7 boost its own targets for delivering vaccines to the emerging world.

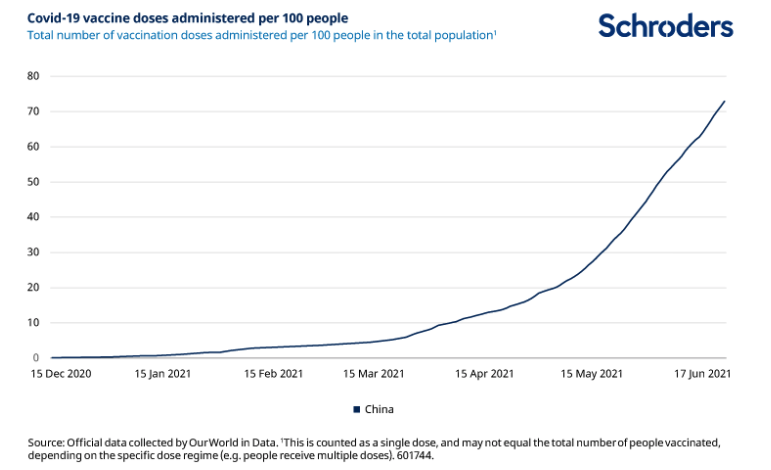

The pace of vaccinations in China has accelerated sharply

China is now rolling out Covid-19 vaccines at a blistering pace. According to the National Health Commission, the total number of vaccines delivered broke through the 1 billion barrier over the weekend.

About two thirds of the 1.4 billion population has received at least one dose, and the government aims to have fully vaccinated 40% of the population by July.

It will be difficult for the authorities to sustain this rapid rate of inoculations, which has seen it deliver roughly 20 million shots per day in the past week, as the roll-out moves into less urban areas.

But it seems that the government is on track to meets its previous official target to vaccinate 80% of the population by the end of the year much more quickly than anticipated. Indeed, at current rates the target could be met at some point during the third quarter.

That should be good news for China.

Could this provide a modest boost to domestic consumption?

The rapid roll-out of vaccines should ease concerns about low levels of natural immunity in China. The government’s robust handling of Covid through strict lockdowns last year virtually eradicated new, domestically transmitted cases of the virus within two months of the outbreak being officially reported.

But it also meant that China built up very little natural immunity. As has been seen in other countries around the world that have handled Covid through containment, this has left populations and economies vulnerable to fresh outbreaks particularly of new, more infectious variants.

Meanwhile, the faster roll-out of vaccinations may give some marginal support to the recovery in consumer spending, which has so far lagged behind the broader economic rebound. Relatively sluggish consumer activity probably reflects some structural shift in economic activity, for example in remote working, along with an apparent absence of a strong recovery in the labour market. But to the extent that hesitancy regarding Covid has been a headwind for consumption, this should fade as the vaccination rate climbs.

Why this is also good news for broader emerging markets

China’s vaccine boom should also be good news for the rest of the world. The implication of China meeting its domestic vaccination targets more quickly than anticipated is that it might not be long before it begins to export large numbers of shots to other EM that have so far been starved of reliable supply.

As we noted earlier this year, both China and Russia were likely to try and fill the vaccine vacuum in EM caused in large part by hoarding in developed markets. China in particular had at the time already agreed to supply its home-grown vaccines to most countries in Africa and Latin America along with parts of Asia and Europe.

Concerns about vaccine diplomacy could also see other countries respond by offering more shots to EM. The US announced last month that it would prioritise sending vaccines to parts of Latin America after China provided deliveries of inoculations to countries in the region. G7 leaders announced at the end of their recent meeting in the UK plans to donate 1 billion vaccines over the next year, but could feel compelled to be more ambitious if China does start to ramp-up its exports.

Anything that can speed-up the roll-out of vaccines in EM would clearly be good news for dealing with the global pandemic and slowing the emergence of new variants. And better handling the health crisis could also have some positive spill over to the economic outlook and performance of assets in the emerging world.

– For more visit Schroders insights and follow Schroders on twitter.

Topics:

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.