What are “accidental savers” doing with their surprise savings?

Lockdown restrictions have curbed spending, resulting in higher savings in the UK. Some of this has found its way into the financial markets; actively managed responsible investment funds have been the biggest beneficiaries.

The words “accidental” and “saver” don’t often appear in the same sentence together. Saving usually takes some effort and requires sacrifices and discipline. However, the lockdown changed this for some people.

How the pandemic has reduced workers’ expenses

A quirk of the pandemic so far is that, for some, income has remained largely unchanged while expenses have fallen. Commuter coffees and lunches, gym memberships, holidays and train fares, restaurant and pub spending, are costs that all-but disappeared overnight in many places, making some people inadvertent savers.

A typical household in the UK spends an average of 22% of their usual weekly budget on activities that were mostly ruled out under lockdown, the Office for National Statistics (ONS) found. Other research shows that almost 40% of Britons report saving more since the imposition of social-distancing constraints.

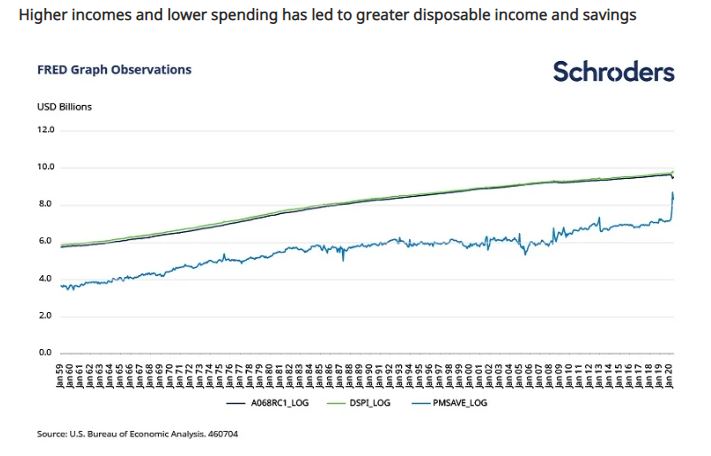

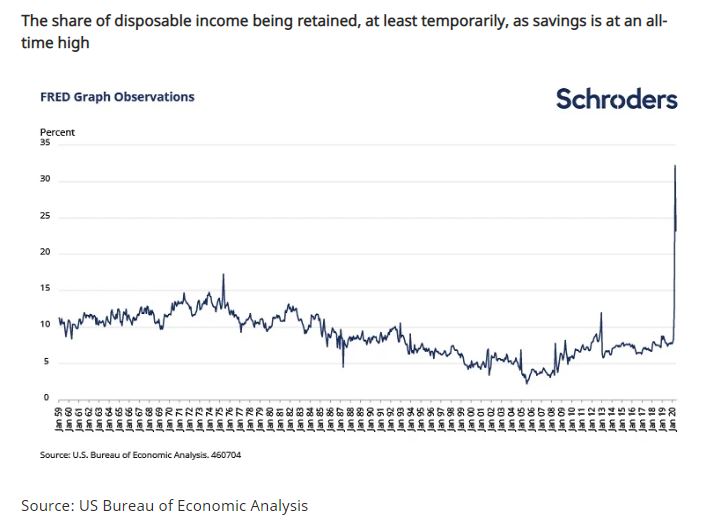

In the US, the data paints a similar picture. The first chart below shows shows how federal aid has boosted incomes at the same time as spending has fallen, resulting in greater disposable income and higher savings. The second chart shows that the personal savings rate hit a record 33% in April. This represents the percentage of people’s incomes left after they pay taxes and spend money.

Saving vs investing

We’ve also seen unprecedented demand for trading accounts. Given low interest rates around the world, it isn’t that much of a surprise that people with extra cash might look to the financial markets to generate returns.

A number of investment platform providers report a dramatic pick-up in new account openings and trading activity since the outbreak of the coronavirus; growth in new accounts has been in excess of 100% in some cases in the UK. Robinhood, the stock trading app apparently favoured by millennials, saw an astounding 3 million new accounts opened in the first quarter.

Sheila Nicoll, Head of Public Policy, said:

“It is a welcome development if people consider putting some of their savings to good use by investing in capital markets. But we can’t tell yet from only a couple of months of activity whether this is a one-off fad rather than a conscious decision to make long-term investments.

“The reality is that people don’t think in terms of “investment products”; they seek solutions to their real life problems. We need to ensure that they have the tools they need to view investing as a way to achieve their financial aspirations. This involves understanding the risk of not taking risk as well as the value of riding out short-term turbulence in the market, such as the one we have been experiencing in the last months.

“Creating such a culture of investing is not without its challenges. While there is no silver bullet, the recommendations by the High Level Forum on the EU Capital Markets Union, on how to encourage people to invest in capital markets should bring us closer to this goal in Europe.”

For more:

– Watch: Is Big Tech under threat?

– Read: Peter Harrison: UK business needs a £30bn equity injection

– Learn: Why old market trends die hard

How people are investing: shares and sustainable funds

Many investors used the market weakness in March to scoop up shares. Stocks like the FAANGs (Facebook, Amazon, Apple, Netflix and Google) have been the prime beneficiaries of this increased trading activity. They have led the sharp market recovery since the Covid-19 collapse, taking their valuations back to elevated levels.

But retail investors have also been piling into funds.

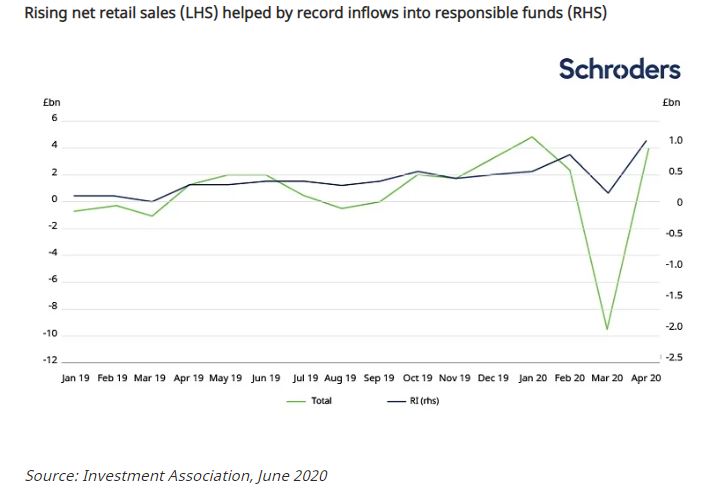

After record outflows of £10 billion in March, net retail sales of UK-authorised funds have bounced back to £4.2 billion in April, according to data from the Investment Association. Investors showed a clear preference for actively managed funds, with active net retail sales (£2.7 billion) double that of passive sales (£1.4 billion).

The data suggests that responsible investment funds were a particularly popular choice in both the US and UK. April saw investors buy a record £969 million in UK-authorised funds that are either managed with a sustainability theme, apply exclusions or are classified as impact funds.

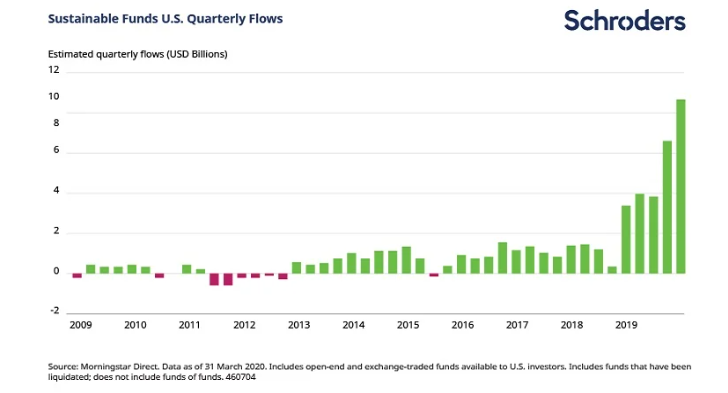

It’s been a similar story of record flows for US sustainable funds. Estimated net flows $10.5 billion in the first quarter, easily surpassing the previous quarterly record seen in Q4 2019.

Why sustainable funds?

Sustainable funds have not just seen impressive inflows; they have also been performing well, putting paid to naysayers’ concerns about a performance trade-off.

Research by Morningstar shows that close to six out of 10 ESG-related funds beat the returns generated by their more conventional, or non-ESG-focused counterparts in a sample of 745 Europe-based sustainable funds. This has been the case over the last one, three five and 10 years and, most recently, during the coronavirus crisis which saw sustainable funds outpace “traditional” funds by up to 1.83%. They also have better survivorship rates; on average, more than three-quarters of ESG funds that were available 10 years ago still exist today, compared with less than half of traditional funds.

Clearly the crisis is turning the spotlight on sustainable investing and increasing both the visibility and perceived importance of sustainable business practices. Although sustainable investing was becoming an increasingly popular choice among investors before the crisis, the events of 2020 seem to have accelerated the trend towards investing with a conscience.

Andy Howard, Global Head of Sustainable Investment, said:

“The crisis has hammered home the ties between companies and the societies in which they operate, underscoring the need for a new social contract. It may just provide the catalyst to the systemic change needed to address mounting social and environmental pressures.

“Climate change, inequality, access to healthcare and employee protection are all issues that have been attracting increased attention for many years. The crisis has served to highlight that they urgently need tackling.

“That investors are choosing to put their savings into companies and funds providing solutions to those problems is a clear sign of their appetite to align their investments to their concerns.”

What are the risks?

Past performance is not a guide to future performance and may not be repeated.

The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

If you are unsure as to the suitability of any investment speak to an independent financial advisor. This information is not an offer, solicitation or recommendation to adopt any investment strategy.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.