The Notebook: Rupak Ghose on the FTSE’s struggles, Goldman Sachs morale and the ludicrousness of LinkedIn ‘extreme CEO’ routines

Where interesting people say interesting things. Today it’s Rupak Ghose, an adviser to fintech companies and a former analyst

The FTSE needs a magnificent seven

TheUK stock market is unfashionable. Low growth. Low ambition. Political risk of an emerging market. More attractive tax-efficient Gilt yields. And too small for the rest of the world to worry about. So, what can government and shareholders do about it?

There are lots of sensible ideas being discussed around pension funds, startup investing, stamp duty abolition and other structural reforms. None of them are likely to address our biggest birth defect, the lack of large tech stocks. Any slim hope went up in flames with the loss of Arm – albeit this may have been a poisoned chalice given its low growth.

The US stock market has been powered by seven stocks – Nvidia, Tesla, Apple, Amazon, Meta, Alphabet and Amazon – this year. The theme of mega caps driving US stocks is a multi-year one. But we shouldn’t forget that other countries without technology giants have seen their stock markets also outperform the UK owing to a narrow leadership. France and its luxury goods giants are a case in point.

The boardroom of UK PLC must prioritise growth and shareholder returns over box ticking and opaque stakeholder capitalism.

The FTSE 100 with a market cap of £2trn is a small index. Mid-size countries (like the UK) rely on a narrow leadership to their stock markets with most of these multinationals earning the majority of their revenues overseas. We shouldn’t underestimate how a series of Astrazeneca-type success stories – the company’s share price has trebled over the last decade – could change the sentiment of international investors who are currently heavily underweight in the UK. There is also a halo effect to the local economy as in most cases mega caps do tend to have more R&D investment and high paying employment in the country they are headquartered in than they otherwise would.

The UK can’t ignore the huge support other Western governments are giving to local R&D investment. And the boardroom of UK PLC must prioritise growth and shareholder returns over box ticking and opaque stakeholder capitalism.

Payments firms look for growth

Leading merchant acquirer Adyen has seen its share price halve over the last month owing to a profit warning around slowing growth, increased competition and rising costs. The payment space that was the centre of the fintech growth story and the darling of the venture capital industry has seen its share prices crumble over the last 12-18 months.

Over $600bn has been wiped off the valuation of the largest 10 merchant acquirer payments firms. This will be a major headwind for any IPO of Stripe or Checkout.com and for private fund raisings in the space. Investors are questioning the barriers to entry, scalability and growth opportunities of these firms.

What it all comes down to: envy

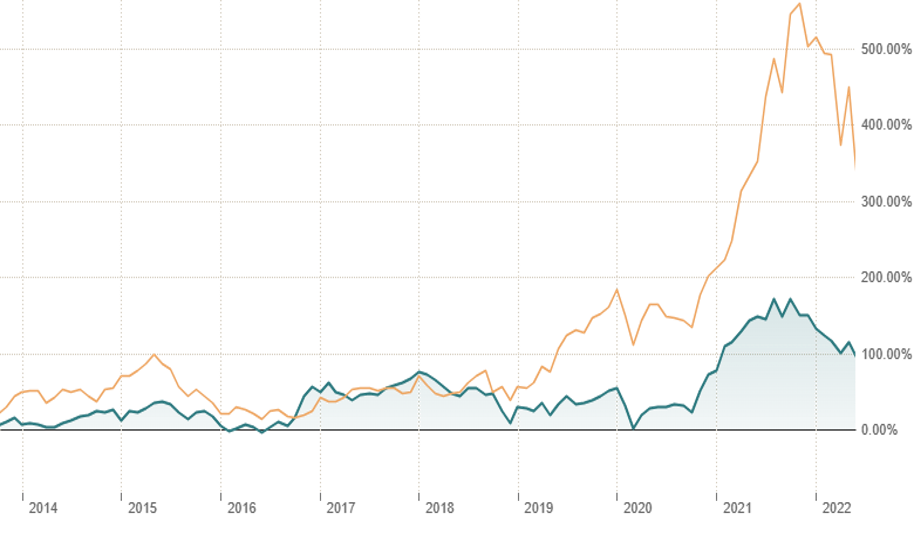

Much has been written about the morale of Goldman Sachs partners and how they don’t like their CEO David Solomon. The puzzle is that Goldman has performed well relative to most of its banking peers despite its consumer banking missteps. Perhaps the answer is most easily explained by the relative performance of the private equity, hedge fund and electronic market maker firms during Solomon’s reign.

Is it merely as simple as Goldman partners who are paid millions of dollars per year envying the even greater amounts of money made by their former colleagues, friends and clients in these more lightly-regulated segments? Goldman (blue in the below chart) used to track Blackstone – but it has materially diverged, downwards, since Solomon took the job.

Ice bath at 5am anyone?

Social media influencers -and let’s face it most media outlets – love a good ‘extreme CEO’ story, whether they’re getting up at 5am and running 10 miles or jump in an ice bath with a sleep is for wimps book. This old chestnut has been rolled out even more than usual this summer. For all those normal people panicking, don’t worry: neither of the zillionaire cage-fighters Zuck or Elon are known to get up early.

I also find it amusing that these articles cite CEOs but never talk about cleaners or road sweepers that get up before dawn. My favourite example is self-help guru Arianna Huffington (pictured) who wakes up based on her own internal body clock and then practises yoga and meditation. All those parents out there as we start the new school term don’t forget your morning yoga and meditation when you are shouting at the kids to get dressed or doing the school run.

Rupak Ghose tweets at @ghose77