Insolvency hits 12-month low as firms thrive

BUSINESS insolvencies fell in August compared with the same month in 2012, marking 12 months of falling insolvency rates, according to data out today from credit information firm Experian.

A total of 1,632 firms failed in the month, down on the 1,723 that failed in August 2012, and the 12th month in a row that the figure has remained stable or fallen.

“We haven’t seen such a prolonged period of stability and improvement in insolvencies for a while and the figures signal an increasingly robust business population, which bodes well for growth,” said Max Firth, managing director of Experian Business Information Services.

“What is particularly significant is the biggest fall coming from 51 to 100 employee companies.

“It follows on from a strong year-on-year drop in July and will give more confidence to these mid-sized businesses which suffered the most during the recession.”

Medium-sized businesses with between 51 and 100 employees saw insolvency rates fall from 0.19 per cent in August 2012 to 0.14 per cent in 2013.

The largest companies with more than 500 employees fared worse, with insolvency rates jumping from 0.06 per cent in August 2012 (five insolvencies) to 0.17 per cent this year (15 insolvencies).

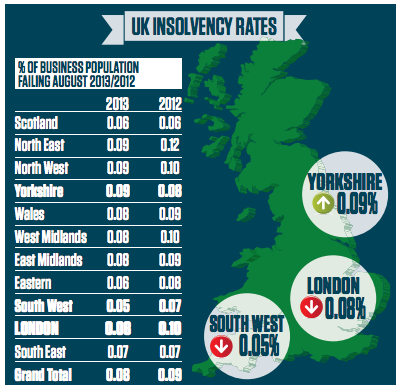

August’s overall insolvency rate for the UK fell from 0.09 per cent in 2012 to 0.08 per cent in 2013, with the South West reporting the lowest insolvency rate of only 0.05 per cent.

Yorkshire was the only region to see a slight increase in insolvency in August, from 0.08 per cent in 2012 to 0.09 per cent this year.

In London, the insolvency rate last month was at 0.08 per cent (accounting for 447 insolvencies) down from 0.10 per cent in August 2012.

Of the UK’s five largest sectors, the building and construction industry, saw the largest fall in insolvency rates, from 0.17 per cent in August 2012 to 0.12 in August this year.

The insurance industry saw the largest fall overall, from 0.15 in August 2012 to 0.03 in August this year.