How does geopolitics impact investment returns and what can you do about it?

Geopolitics can significantly impact investment returns; whether it’s trade wars, actual wars, populist politicians or terrorist attacks.

And as we discussed earlier this year in our “Inescapable investment truths for the decade ahead”, geopolitical risks are on the rise and will play a major role in the years to come.

So, what does this mean for investment performance and how might investors respond?

What do we mean by geopolitical risk?

Geopolitical risk can refer to a wide range of issues, from military conflict to climate change and Brexit. We look at it as the relationships between nations at a political, economic or military level. The risk occurs when there is a threat to the normal relationships between countries or regions.

How does geopolitical risk affect economies?

Geopolitical risk creates uncertainty. This weighs on economies and financial markets as decision-makers hold off from making major commitments.

Firms delay investment decisions or new hires. Consumers delay spending on big-ticket items such as cars or houses. Financial investors delay their decisions as they await clarity.

How does it affect markets?

Geopolitical risks tend to trigger investors to move away from riskier assets like shares and towards perceived “safe” assets.

This negatively impacts stock market returns, while government bonds benefit (particularly those with short maturities as they are perceived as the safest).

Geographically, investors also shift their money away from the perceived riskier regions such as emerging markets and towards developed markets like the US.

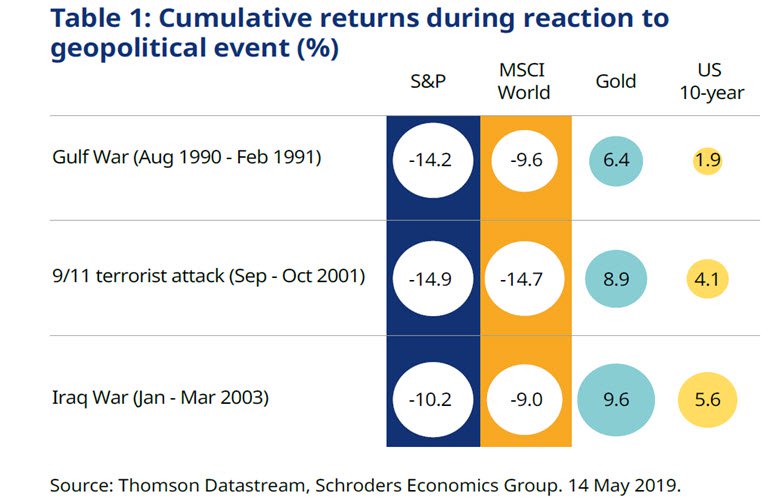

This is illustrated below, by the performance of four different assets (US shares, global shares, gold and US government bonds) during three major geopolitical events.

How did our analysis work?

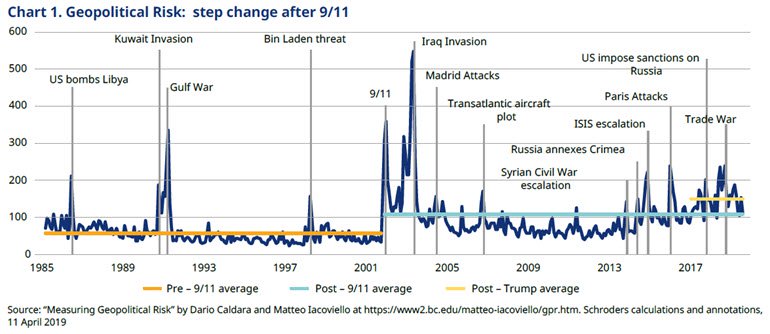

Our economists Keith Wade and Irene Lauro looked at five different periods of heightened geopolitical risk since 1985.

To do this they used the Geopolitical Risk Index (GPR), which reflects automated text search results of the electronic archives of 11 national and international newspapers. It captures the number of mentions of key words such as “military tensions”, “wars” and “terrorist threats”.

We defined periods of geopolitical risk as whenever that index went above the 100 mark, which you can see below.

Our economists created a “safe” and a “risky” investment portfolio and compared their performances during these periods.[1]

Of course, no investments are truly “safe” or risk free. Investment values go up and down and you don’t always get back the amount you originally invested.

We use the term “safe” merely to distinguish between the relative stability of assets like US government bonds (which the US government is highly unlikely to default on) versus shares, which are relatively “risky” (companies regularly go bust). We could equally have called them “less volatile” and “more volatile” portfolios.

What did our analysis show?

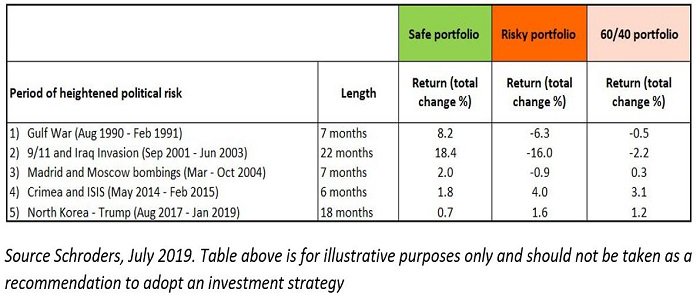

Our analysis shows that in the short-term the portfolio of “safe” assets delivers higher returns than the risky portfolio in three out of the five periods considered.

When the returns were “risk-adjusted”, this was also the case. Risk adjusted returns refers to the Sharpe ratio, which measures the return of an investment compared to its risk.

We also looked at how a diversified “60/40” portfolio (60% risky assets and 40% “safe” assets) compared. We found that it performed worse than the “safe” portfolio (both in total returns and risk-adjusted).

What if you extend the time period to until after the geopolitical risk subsides?

The results were particularly interesting when our economists extended their analysis to six months after the GPR index falls back below 100. This enabled them to get a better idea of how an investor would have performed if they had held onto their risky portfolio through the turbulence and then allowed markets to recover their poise.

They found that over the extended time period the risky portfolio outperformed the safe portfolio in four of the five periods (the exception being 9/11 and the Iraq invasion). The risky portfolio also scored better than the safe portfolio in risk-adjusted terms in each of these four periods.

However, an investor would have had to withstand considerable volatility to realise the benefits of the risky portfolio so we threw into the mix a “dynamic” portfolio. This would involve an investor implementing a safe portfolio as soon as tensions start to rise (the GPR goes above 100) and switching to the risky portfolio when they dissipate (goes back under 100).

For an individual investor this would likely not be practical with their own portfolios. However, it’s likely the best option for those who entrust an active fund manager that takes geopolitical risk into account.

This dynamic portfolio did well, delivering a higher return (both total and risk-adjusted) than the risky portfolio in three out of the five periods and higher than the safe portfolio in four out of the five periods. The analysis showed that active fund managers can potentially avoid some of the losses and still enjoy much of the benefits from taking geopolitical risk into account.

Keith Wade, chief economist at Schroders, said: “There has been a significant increase in geopolitical risk during the Trump presidency. The emergence of China as a global superpower and the rise of populism means this is unlikely to change soon. We have seen this in the recent breakdown of talks between the US and China: tensions between the two nations remain high and the GPR index remains elevated.

“It is also the case that the scope for central banks to ease monetary policy and provide support to markets as an offset to heightened political risk is less than in previous episodes, given the low level of interest rates and size of central bank balance sheets. Consequently, taking geopolitical risk into account when choosing portfolio strategy will be increasingly important for investors.”

Read more:

- The bias of UK investors that could lead to lower returns

- Ten things every investor needs to know about offshore wind power

[1] The safe portfolio allocates 50% to the US 10-year benchmark government bond, with the rest equally distributed among gold, Swiss franc and Japanese yen. The risky portfolio comprises 50% in the S&P 500, the rest allocated evenly between the MSCI World and MSCI EM Equity indices. After 2007 we also include a basket of local EM sovereign debt made up of local currency sovereign bonds of Turkey, Brazil, Mexico, Russia and South Africa.

Important Information: The views and opinions contained herein are of those named in the article and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This communication is marketing material.

This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 1 London Wall Place, London, EC2Y 5AU. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.