Forward guidance is crumbling – what comes next?

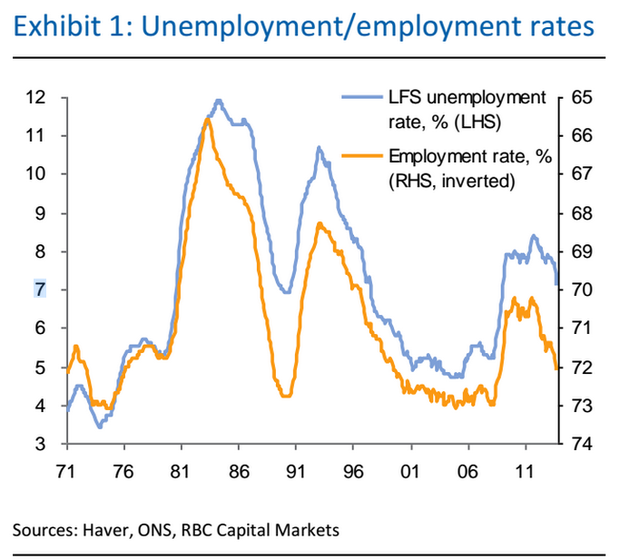

Two years ahead of the Bank of England’s original schedule, forward guidance is circling the drain, with unemployment now within 0.1 percentage points of the threshold for reconsidering a rate hike.

With productivity and wage growth still much diminished, and without significant improvements to exports or investment, the Bank is expected to alter forward guidance to accommodate the rapidly improving labour market. How might that happen?

Lower the threshold

The MPC could simply decide to say that its threshold was too high, and lower the related rate to 6.5 per cent. The Bank chose unemployment specifically because it is a reliable, well-understood figure, and so a simple threshold cut is superficially appealing.

However, a cut might damage the MPC’s credibility, especially if unemployment continues to fall and further cuts to the threshold are needed again in the future.

Wage-related guidance

EY’s Item Club suggested this week that forward guidance be re-tooled to take into account wage growth, which has been muted despite the rapid fall in unemployment.

The Bank could choose to make an interest rate hike contingent on wage growth outstripping inflation, which some analysts expect to happen later this year.

Do nothing

The Bank doesn’t actually have to alter guidance at all.

Having made clear that it is not mandated to raise rates when unemployment falls to seven per cent, the Bank could simply go back to month-by-month decision making, based on an inflation target of two per cent, allowing markets to make of that what they like.

Berenberg’s Robert Wood has suggested this:

The labour market has tightened, firms are reporting rapidly rising recruitment difficulties, and some surveys report rising wage pressure. Wage growth, in particular, is coming from very subdued levels. Inflationary pressure remains subdued for now. But lowering the unemployment threshold would unnecessarily tether the BoE to a dangerously low target.

Back to the start

When Mark Carney announced the decision to introduce forward guidance, he offered a number of options that had been considered.

These inlcuded the time-contingent guidance that he instituted at the Bank of Canada, pledging to hold interest rates until a specific date.

Other candidates for data-driven guidance were measures of the output gap, nominal gross domestic product (NGDP) and real gross domestic product (RGDP), all of which were rejected.

While it’s unlikely that the MPC will go back to the drawing board entirely, they may be regretting their chosen indicator now.