Rachel Reeves – “Gilty” as charged

The verdict is in. The Gilt market has found the Chancellor Rachel Reeves guilty of reckless endangerment of the country’s finances.

A large electoral majority led her to think the world would happily finance what she described in her Mais Lecture as the “smart and strategic state”.

Sticking to fiscal rules is for nought if the market doesn’t believe you can ever reach your high-growth destination.

The UK now faces the sentencing of higher interest rates on an already high pile of debt. Debt interest payments were forecast by the OBR to average £112bn a year between now and 2030, even before the latest increase in yields, compared to just £25bn in 2020-21.

Should a doom loop follow, where spiralling higher interest rates lead to even higher debt interest payments, Judge Starmer will have no choice but to get out his black cap.

The market doesn’t care that her predecessors committed similar crimes. If anything, there were high hopes that she would be different and that her “Securonomics” would bring boring stability.

Instead, the self-confessed girlie swot took a massive gamble in her first Budget.

Borrowing more and taxing more to spend more left her – and UK assets – hostage to fortune. Any increase in yields, whatever the cause, would reveal that Rachel Reeves’s plan had increased the vulnerability of the UK’s fiscal position.

Borrowing for growth

The Chancellor chose to borrow more in the short term to invest for the long term. This plan can work if those funding you believe the plan will come to fruition. But seven months in government has only brought negative consequences: stagnant growth, sticky inflation, reduced job vacancies and depressed consumer and business confidence.

With a fresh new government coming into the US on a reflationist agenda, the market is sceptical that a high-spending unproductive British state can reverse the UK’s malaise. As one investor put it in the autumn, “Why should I finance pay rises for ASLEF?”.

No doubt the government would argue it just needs time. But Rachel Reeves’s decision to run with only a tiny sliver of fiscal headroom against her self-imposed fiscal rules hasn’t given her enough breathing space.

Governments often complain they pull levers and nothing happens. One of the few that has an immediate impact is changes to tax policy. Consumers and businesses immediately alter their behaviour in the face of different incentives.

The rise in employer national insurance contributions and lowering of the threshold for its payment has already forced businesses to reconsider their hiring plans ahead of its implementation.

Meanwhile, the laudably transformational but far more intangible reform of the planning process will take years, if not decades, to bear economic fruit.

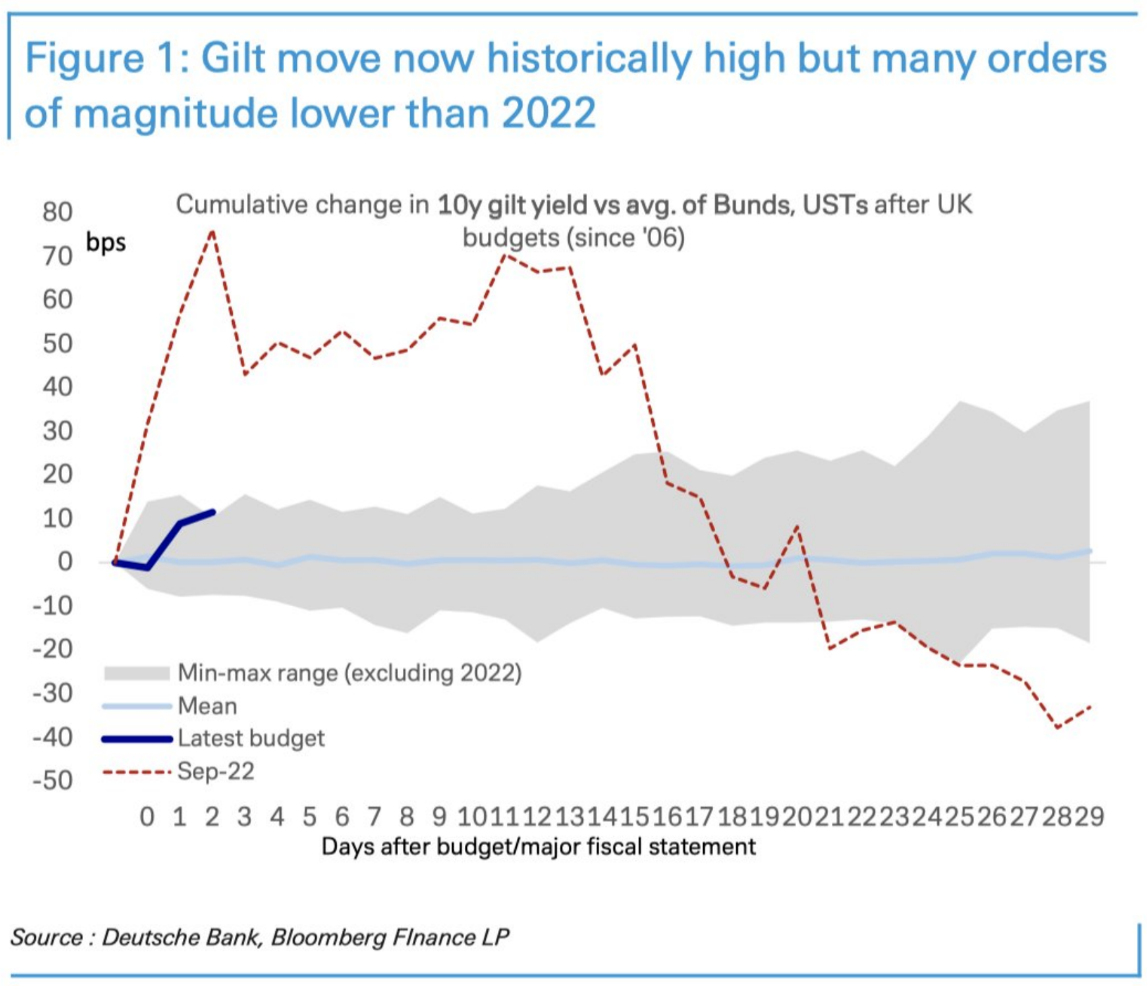

Investors were already sceptical in the immediate aftermath of the Budget. Absent the Truss episode, the Rachel Reeves budget would have delivered the biggest two-day increase in 10y gilt yields of any budget since 2006, as this chart from Deutsche showed:

At the time, in a bid to put the moves into context, Treasury Minister Darren Jones concluded ‘we’ve all got Liz Truss PTSD’. This deep desire to avoid being Liz Truss now risks further compounding the problem for the government.

Keeping the OBR happy does not necessarily keep the markets happy. A Chancellor must retain the confidence of the markets or face the cost of a permanently increased political risk premium on UK assets. This is a penalty such an indebted country can ill afford.

So far, the government is wildly behind the curve.

Tough choices for Rachel Reeves

In response to the sell-off in Gilts and Sterling, the Treasury issued a statement which said ‘only the OBR’s forecast can accurately predict how much headroom the government has, anything else is pure speculation’. Setting aside the OBR’s less than stellar forecasting record, this is wilful ignorance of how markets work.

Every moment of every day the market speculates – or rather judges – the price of assets. They will not wait for the OBR to release its updated forecast on 26th March 2025 to determine whether the government has a credible plan. They are saying right now that the plan is too risky in a world of higher interest rates.

Rachel Reeves has said she won’t be announcing any new fiscal measures until her next Budget in the Autumn. That is now untenable. Unfortunately, her room for manoeuvre is minimal.

Ripping up the budget is politically impossible. Raising taxes further would harm growth so it’s economically impossible. Borrowing more would be adding fuel to the flames so it’s financially impossible. Hence the market has inferred spending cuts are the only solution.

This will not happen without a massive, possibly existential, fight within the Labour Party. Cabinet ministers were already writing to the Prime Minister to complain about tight budgets in October. The Spending Review has had to be pushed back to June. Having complained of fourteen years of evil Tory cuts, the Labour Party could not survive anything that even hinted of austerity.

The Labour Party has a huge majority, but it does not have a mandate. This is what bedevilled Truss – but the PTSD with that era ends there. Waiting for the OBR to calculate a number to put into Reeves’ spreadsheet will not save this government from further falls in Gilts and Sterling.

A rational repricing of UK government debt means the market has concluded Rachel Reeves has made the wrong diagnosis and delivered the wrong solution.

This isn’t an election campaign. This is government. Once you lose the confidence of the markets, it’s gone. If Reeves won’t change, Starmer will have to change the Chancellor. Guilty as charged.