What does Meggitt’s bid premium tell us about UK shares?

Have you ever wondered why there has been such a marked pick-up in the amount of UK businesses that have been bid for in recent years? This year is no exception, and has been an extremely active one, with a record number of deals in the first half of 2021.

And there is no sign of this momentum slowing. Earlier this month, Meggitt, the UK-based aerospace and defence equipment supplier, received a bid from Parker Hannifin in the US at a whopping 71% premium.

That has since been followed by another takeover approach, this time from US group TransDigm, potentially with an even higher offer.

What is most striking is Parker Hannifin’s expectation of the return it could potentially deliver on the transaction. With mergers and acquisitions (M&A) usually a zero-sum game between buyer and seller, this deal has made us stop to ask – what is really going on with the UK stock market?

Steep discounts across the board

How is the M&A market for UK listed shares so hot, while global asset allocators tend to show such indifference toward the market? We see a number of reasons, with the most obvious being that the UK lacks large cap technology companies in its benchmark.

Clearly, this would provide partial explanation as to the relative undervaluation. However, there is another less obvious reason: fund flows.

Since Brexit, and its five-year reign of uncertainty over everything from the hard currency status of sterling to the trade relationship with Europe, the asset class has suffered large and sustained outflows.

Global investor allocations to UK equities have almost halved since late 2015, and the asset class has seen 25% cumulative outflows since June 2016, according to Refinitiv Lipper data. The impact on the UK stock market has been profound, leading to an underperformance (in US dollar terms) not seen since the early 1970s.

Remember, the 1970s were a period of stagflation (slow economic growth and rising inflation) when the country was often in a state of emergency, culminating in the “Winter of Discontent”.

Discover more at Schroders insights or click the links below:

– Video: 32 reasons not to invest in the stock market

– Podcast: The plastic problem facing investors

– Read: Does the IPCC report change anything?

We would highlight that the relative “cheapness” of the UK stock market compared to other developed markets such as the US and Europe is more persistent and pervasive than commonly understood.

The cheapness is not just a function of ”value” versus the “growth” styles of investing, or lack of exposure to top-performing technology companies.

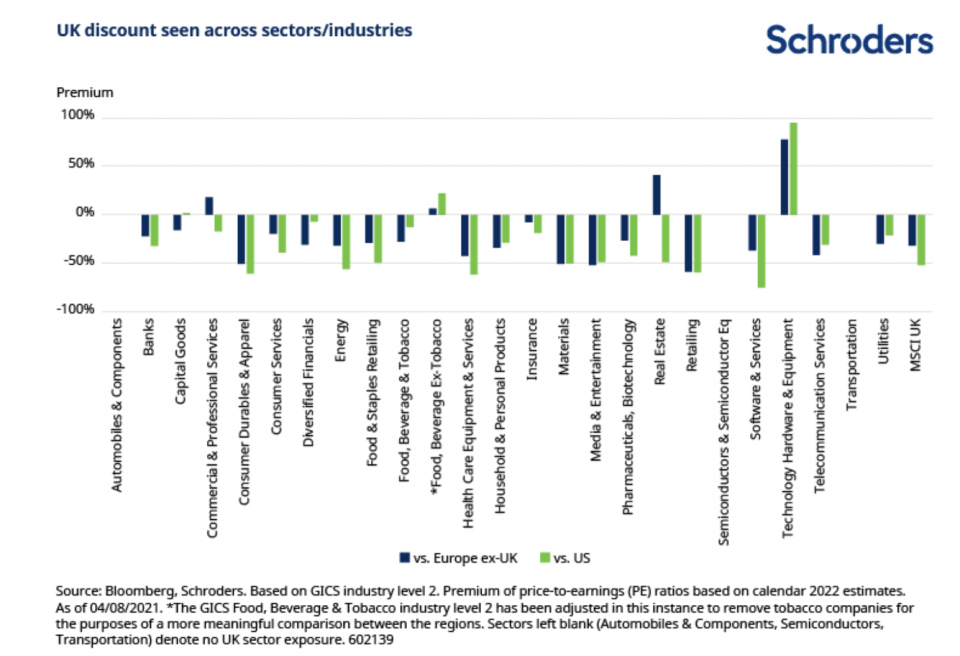

While this is some of the story, it does not explain the steep discount across sectors/industries versus both the US and Europe (see first graphic, below) causing acquirers to congregate as a flock around the UK.

Of course the analysis above is subject to differences in growth prospects, quality or those instances where sectors/industries are dominated by large stocks with outlier valuations (particularly in the US).

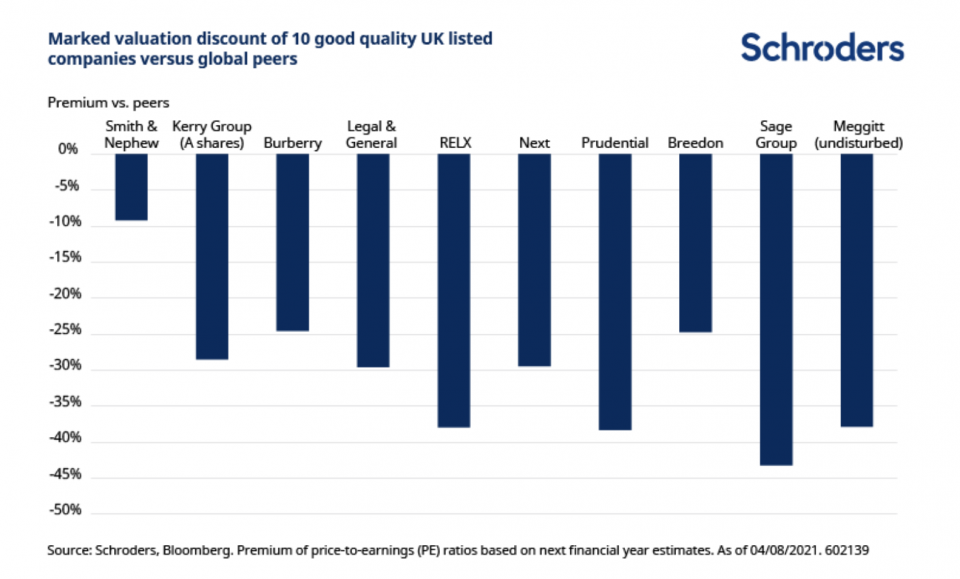

For this reason, we have also selected 10 diverse good quality companies and benchmarked their valuations versus their most relevant global peers (see below). The peers operate in the same lines of business and rank similarly in terms of growth and on measures of quality, such as profitability and returns.

The UK discount is evident in this analysis too – and, in fact, we were surprised by the outcome. For interest, we include Meggitt here at its “undisturbed” valuation before the Parker Hannifin bid.

Discount due to location of listing

This group of stocks are on average growing their top line at an 8% compound annual growth rate (CAGR) between the financial years 2021-23 and earnings per share by 13% CAGR.

The comparative aggregate figures for the peer group are similar at 8% and 15% respectively.

With this group of stocks there isn’t a growth problem or a quality problem. In fact, many are leading industry players or have unique business models.

The discount in our view largely arises from where they are listed and the resulting fund flows.

Record levels of UK M&A in 2021 to date and the significant bid premium for Meggitt have an important message for investors. This is that other market participants such as private equity or trade buyers will step in to address discounts if listed equity markets fail to recognise value.

As the well-regarded investor Peter Davies of Lansdowne Partners said in a recent interview:

“…the global investor is viewing the UK through a rear-view mirror of political risk rather than a prospective mirror of it…systemically a UK exposed company will be trading at a big discount to its peers in any part of the world.”

We would concur with these words which highlight the attractive backdrop for UK equities over the next couple of years. In our opinion, these words are one of the best summaries out there for what’s really going on with the UK stock market.

This article was published in August 2021. Any company references are for illustrative purposes only and are not a recommendation to buy and/or sell, or an opinion as to the value of that company’s shares. The article is not intended to provide, and should not be relied on, for investment advice or research. If you are unsure as to the suitability of any investment, please speak to an independent financial adviser.

– For more visit Schroders insights and follow Schroders on twitter.

Topics:

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.